국제신용평가사 피치가 12일 밤 한국 은행들의 '스트레스 테스트' 결과를 발표, 큰 파장이 일고 있다. 특히 피치는 개별은행들의 테스트 결과까지 함께 공개해 정부당국과 관련 은행들의 강한 반발을 사고 있다. 그러나 이 보고서는 이미 세계에 배포된 상태다.

보고서는 올해 우리나라 경제성장률을 -2.5%로 잡고 있다. -4%를 전망한 IMF보다도 후한 점수를 주고 있는 셈. 그럼에도 불구하고 피치의 테스트 결과는 충격적이다.

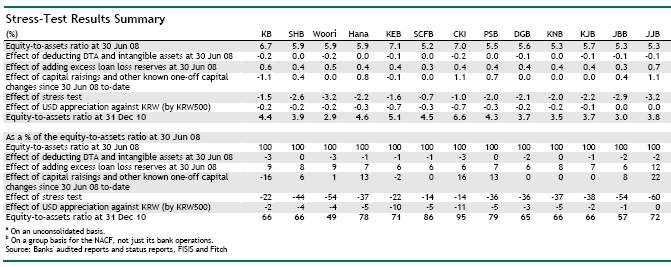

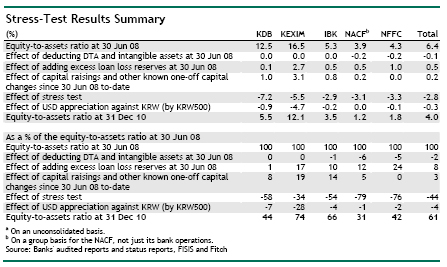

피치는 내년말까지 건설사 도산 등에 따른 대출자산 손실(Credit loss) 및 유가증권 투자손실 증가, 환율상승에 따른 자산증가 등에 따라 42조원 규모의 신규손실(자본감소) 발생하고, 이로 인해 은행 건전성을 체크하는 핵심 기준인 '단순자기자본비율(equity-to-assets ratio)'이 2008년 6월말 6.4%에서 2010년말에는 4.0% 수준으로 하락할 것으로 추정했다.

특히 평균 4%에도 못드는 은행들 가운데에는 농협, 수협은 1%대라는 최악의 수치를 보이고 있으며, 우리은행은 2%대, 그리고 대구, 경남, 광주, 전북, 제주 등 지방은행들과 신한은행이 3%에 들어 충격을 안겨주고 있다.

상당수 은행이 공적자금 투입없이는 존립이 힘든 위기 상황에 몰릴 것이란 의미다.

다음은 <뷰스앤뉴스>가 긴급입수한 피치 보고서의 원문 전문.

Stress Test on South Korean Banks

Background and Summary

On the back of the global economic downturn, South Korea’s export‐oriented economy is expected to contract in 2009 by around 2.5% (versus growth of 2.5% in 2008 and 5.1% in 2007). Growth in 2010 is also likely to be weak. As a result, credit costs for Korea’s banks are, and are likely to continue, rising (the system‐wide NPL ratio increased to 1.11% at 31 December 2008 from a low of 0.70% at 30 June 2008).

This is particularly so given the banks’ quite strong loan growth in the years leading up to the downturn, much of it to relatively higher risk SMEs (versus say mortgages and large corporates), which points to a general level of overinvestment. Loans were especially brisk for construction companies, which have been under notable strain for some time now due to an excess of supply after overbuilding in recent years, particularly in regional areas. Meanwhile, exporters of both consumer and capital goods (including South Korea’s substantial shipbuilding and related industries) are seeing sharply lower demand from the US, Europe and elsewhere. In addition, a number of sizeable exporters are unable to meet very large losses to the banks arising from being on the wrong side of foreign exchange hedging facilities amidst the recent rapid depreciation of the KRW. Meanwhile, with lower exports, imports are also down, and importers are also being negatively affected, along with non‐hedged USD borrowers, by the sharply weaker KRW. At the same time, all businesses are likely to be affected by tighter credit conditions, in both KRW and foreign currency.

In light of these conditions, Fitch Ratings has tried to evaluate how the capitalisation of individual South Korean banks, and the system as a whole, would withstand a stress scenario over the 2.5 years to 31 December 2010, involving; credit costs at about 7% of loans (versus negligible credit costs in recent years), varying depending on the individual banks’ exposure to higher risk loans such as to construction companies, versus lower risk mortgages; a 30% loss on equity securities holdings (and lower losses on debt securities); lower net and non‐interest income; and finally, some asset growth through the inflation of foreign currency assets given the depreciation of the KRW in the past year (more specific details of the stress scenario and the results are provided below).

In summary, the stress test result in a circa KRW42trn decline in the capitalisation of South Korean banks — ie a reduction in their combined equity‐to‐assets ratio of 6.4% at 30 June 2008 to 4.0%). This is concerning given that the 6.4% level at 30 June 2008 was only just satisfactory in the first place, having declined notably in previous years through the banks’ quite strong loan growth. Furthermore, postcrisis, there is a growing belief that banks should be even better capitalised than they have been historically. On this basis, the South Korean government’s recently announced plan to inject KRW20trn into the banks (through the establishment of a ‘Bank Recapitalisation Fund’ or BRF) may not be sufficient, particularly given that much of this may well only be in the form of subordinated debt, with the balance being hybrid capital of which the details, in regard to term and quality, are yet to be announced.

Fitch would have been inclined towards a harsher stress scenario than that applied, but for the substantial and wide‐ranging measures being adopted by the South Korean government to support its economy and banks. Such measures include a steady reduction in policy interest rates over the past six months (to 2.00% from 5.25%); plans for a KRW51trn (USD34bn) fiscal stimulus package (comprising KRW35trn in tax reductions and KRW13trn in infrastructure and other spending); a KRW3.5trn capital injection into certain policy banks (mainly to enable greater lending to SMEs, which account for the bulk of corporate loans in South Korea’s banking system); the purchase of up to KRW6trn in land and buildings from property development/construction companies; the purchase of up to KRW20trn in problematic assets from the banks; and a KRW20trn increase in government guarantees on SME loans by the banks (to KRW64trn). The latter two items will be of particular and direct benefit to the banks along with the BRF. Notably, Korea’s central bank has also been providing the banks with substantial KRW and foreign currency liquidity support.

Stress Test Assumptions and Rationale

The stress scenario is based on the 2.5‐year period of 30 June 2008 3 to 31 December 2010 and comprises; 1. Credit costs as follows; a. Construction loans, 12%; b. Manufacturing loans, 10%; c. Mortgage loans, 1%; d. Non‐mortgage consumer loans, 8%; and e. Other loans, 6%. Note that these credit cost assumptions have been applied to the banks’ loan books at 30 June 2008 and are for the whole 2.5‐year period (ie they are not per annum) and are after assumptions for recoveries on the sale of collateral and/or loan forgiveness. The relatively high credit costs on construction loans reflect the particular difficulties that the sector is facing, albeit partly offset by a relatively high assumed collateral recovery rate of 40%. Meanwhile, the very low credit costs for mortgages reflect expectations of a relatively low default rate and a high recovery rate as per historical trends in Korea and elsewhere — particularly given the conservative loan‐to‐value ratios at which mortgages have typically been provided in South Korea over recent years. 2. A 30% loss on the value of equity investments given market valuation declines(noting that the Korea Composite Stock Price Index (KOSPI) is actually currently down 33% since 30 June 2008). 3. Credit costs equal to 5% of corporate bond holdings — notably lower than that assumed for corporate loans in general, as corporate bond issuers do tend to be of higher quality. 4. Credit costs equal to 2% of other securities — which is particularly low given that these mainly comprise major, highly rated, foreign currency issuing South Korean corporates and offshore entities. 5. No dividend payouts. 6. A 15% decline in net‐interest income (on that for the 12 months to 30 June 2008 as shown in Appendix 1); while pricing power for the banks is improving, particularly in regard to SMEs, this is expected to be more than offset by higherNPLs (and therefore non‐accrual loans), a low spread on ‘free’ and other lowcost funding given the very low interest rate environment, and a shift towards lower risk, lower yielding investments. 7. A 10% decline in non‐interest income (on that for the 12 months to 30 June 2008 as shown in Appendix 1) given lower volumes in such areas as credit cards, wealth management sales and investment banking.

Prior to applying the above stress test, deferred tax and intangible assets have been deducted from the banks’ equity and asset bases. Also, benefit has been given to the banks for excess loan loss reserves held at 30 June 2008 (when NPLs, at 0.70% of loans, were typically about 200% covered by loan loss reserves) — although some of the banks’ “excess” reserves are in fact required by regulation to cover outstanding guarantees.

At the same time, while nil growth in loans and assets has been assumed for the 2.5‐year period, loans and assets have been increased given the inflation of the banks’ foreign currency denominated loans and assets through the sharp depreciation of the KRW since 30 June 2008 (Fitch has assumed a 500bp depreciation in the KRW against the USD, similar to that which has occurred since 30 June 2008 (KRW: USD rate down to 1,497 from 1,043).

Finally, any raisings of common equity (and/or buybacks) by the banks since 30 June 2008 till now have been accounted for, as have certain other known one‐off charges during this period such as losses on structured security investments and the failure of certain customers to meet substantial foreign exchange hedge obligations to the banks. Fitch, however, has not factored in any further such hedge losses, although these may well be significant for those banks most active in this area, particularly if the KRW continues to depreciate.

Results

First and foremost, Fitch notes that this is a stress test and not a forecast; obviously in reality, the relatively harsh level of credit costs assumed would take considerably longer than just 2.5 years to play out (ie including default, negotiations/court‐processing, and sale of collateral).

As shown, line‐by‐line in Appendix 3, all the banks benefit from an excess of loan loss reserves at 30 June 2008, mostly by around 8% of equity (albeit with NFFC’s excess particularly substantial at 24%, and KDB’s very limited at 1%). Meanwhile, numerous banks benefit substantially from common equity raisings since 30 June 2008, albeit with Kookmin being negatively affected by effectively buying back some of its shares in September 2008 (as part of its arrangements to establish itself under a holding company structure).

In terms of the stress test, banks are negatively affected to varying degrees, often largely depending on the extent to which their loan books are weighted in the higher risk area of construction companies (and to a lesser extent, other corporates) versus lower risk mortgages. Other factors, however, include the level of equity securities held, and the banks’ underlying or pre‐provisioning profitability, particularly in regard to net interest margins. Finally, the negative effect of foreign currency asset inflation is obviously a factor for those banks’ with a significant level of such assets.

In summary, the stress test results in the banks’ combined equity‐to‐assets ratio declining to 4.0% from 6.4%, which in turn was only just satisfactory to begin with, particularly given post‐crisis demands for banks’ to be more strongly capitalised than they historically have been. All in all, the banks’ capitalisation declines by about KRW42trn. Should this come to pass, additional capital raisings by the banks would be required. Given current market conditions, however, such capital may have to come from the government. In this light, the government’s current KRW20trn BRF may not be sufficient, particularly to the extent that it is used to buy subordinated debt and lower quality hybrid debt from the banks rather than better quality core capital.

황우석 박사 물먹이더만 이제 미국에서 줄기세포를 한다고 하지 않은가 하지만 정작 한국은 어떠 했나.... 이제는 한국은 그들의 농간에 넘어가지 말아야 한다 IMF때 그들의 요구대로 김대중 정권은 외국에다 회사 많이 팔아 먹었지 않은가... 수출은 잘되는데 달러가 일방적으로 빠져 나가 버렸으니 그때도 그들의 농간 이었지..